A Tour of pyGAM#

Introduction#

Generalized Additive Models (GAMs) are smooth semi-parametric models of the form:

where X.T = [X_1, X_2, ..., X_N] are independent variables, y is the dependent variable, and g() is the link function that relates our predictor variables to the expected value of the dependent variable.

The feature functions f_i() are built using penalized B splines, which allow us to automatically model non-linear relationships without having to manually try out many different transformations on each variable.

GAMs extend generalized linear models by allowing non-linear functions of features while maintaining additivity. Since the model is additive, it is easy to examine the effect of each X_i on Y individually while holding all other predictors constant.

The result is a very flexible model, where it is easy to incorporate prior knowledge and control overfitting.

Generalized Additive Models, in general#

where

So we can see that a GAM has 3 components:

distributionfrom the exponential familylink function\(g(\cdot)\)functional formwith an additive structure \(\beta_0 + f_1(X_1) + f_2(X_2, X_3) + \ldots + f_M(X_N)\)

Distribution:#

Specified via: GAM(distribution='...')

Currently you can choose from the following:

'normal''binomial''poisson''gamma''inv_gauss'

Link function:#

We specify this using: GAM(link='...')

Link functions take the distribution mean to the linear prediction. So far, the following are available:

'identity''logit''inverse''log''inverse-squared'

Functional Form:#

Specified in GAM(terms=...) or more simply GAM(...)

In pyGAM, we specify the functional form using terms:

l()linear terms: for terms like \(X_i\)s()spline termsf()factor termste()tensor productsintercept

With these, we can quickly and compactly build models like:

[12]:

from pygam import GAM, s, te

GAM(s(0, n_splines=200) + te(3, 1) + s(2), distribution="poisson", link="log")

[12]:

GAM(callbacks=['deviance', 'diffs'], distribution='poisson',

fit_intercept=True, link='log', max_iter=100,

terms=s(0) + te(3, 1) + s(2), tol=0.0001, verbose=False)

which specifies that we want a:

spline function on feature 0, with 200 basis functions

tensor spline interaction on features 1 and 3

spline function on feature 2

Note:

GAM(..., intercept=True) so models include an intercept by default.

in Practice…#

in pyGAM you can build custom models by specifying these 3 elements, or you can choose from common models:

LinearGAMidentity link and normal distributionLogisticGAMlogit link and binomial distributionPoissonGAMlog link and Poisson distributionGammaGAMlog link and gamma distributionInvGausslog link and inv_gauss distribution

The benefit of the common models is that they have some extra features, apart from reducing boilerplate code.

Terms and Interactions#

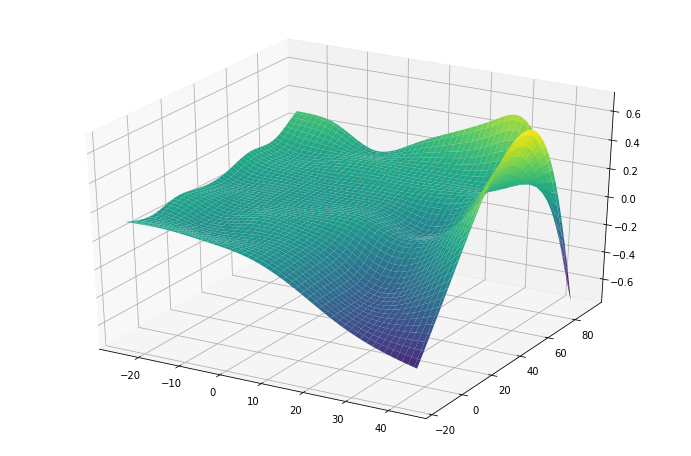

pyGAM can also fit interactions using tensor products via te()

[58]:

from pygam import PoissonGAM, s, te

from pygam.datasets import chicago

X, y = chicago(return_X_y=True)

gam = PoissonGAM(s(0, n_splines=200) + te(3, 1) + s(2)).fit(X, y)

and plot a 3D surface:

[60]:

import matplotlib.pyplot as plt

plt.ion()

plt.rcParams["figure.figsize"] = (12, 8)

[61]:

XX = gam.generate_X_grid(term=1, meshgrid=True)

Z = gam.partial_dependence(term=1, X=XX, meshgrid=True)

ax = plt.axes(projection="3d")

ax.plot_surface(XX[0], XX[1], Z, cmap="viridis")

[61]:

<mpl_toolkits.mplot3d.art3d.Poly3DCollection at 0x7f58f3427cc0>

For simple interactions it is sometimes useful to add a by-variable to a term

[10]:

from pygam import LinearGAM, s

from pygam.datasets import toy_interaction

X, y = toy_interaction(return_X_y=True)

gam = LinearGAM(s(0, by=1)).fit(X, y)

gam.summary()

LinearGAM

=============================================== ==========================================================

Distribution: NormalDist Effective DoF: 20.8449

Link Function: IdentityLink Log Likelihood: -2317525.6219

Number of Samples: 50000 AIC: 4635094.9336

AICc: 4635094.9536

GCV: 0.01

Scale: 0.01

Pseudo R-Squared: 0.9976

==========================================================================================================

Feature Function Lambda Rank EDoF P > x Sig. Code

================================= ==================== ============ ============ ============ ============

s(0) [0.6] 20 19.8 1.11e-16 ***

intercept 1 1.0 1.79e-01

==========================================================================================================

Significance codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

WARNING: Fitting splines and a linear function to a feature introduces a model identifiability problem

which can cause p-values to appear significant when they are not.

WARNING: p-values calculated in this manner behave correctly for un-penalized models or models with

known smoothing parameters, but when smoothing parameters have been estimated, the p-values

are typically lower than they should be, meaning that the tests reject the null too readily.

Regression#

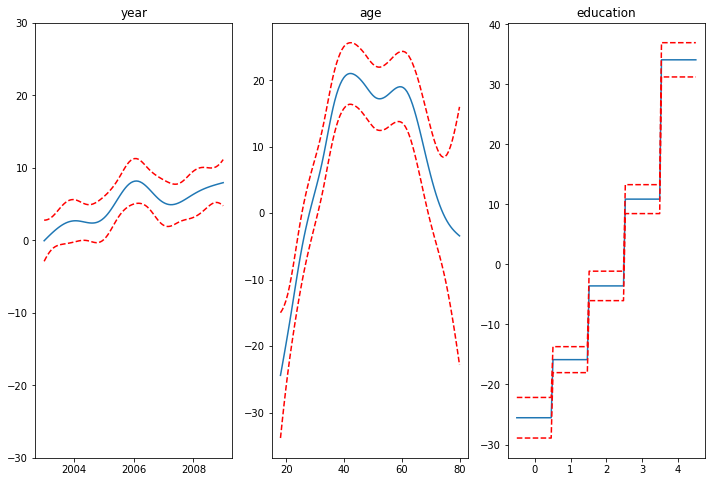

For regression problems, we can use a linear GAM which models:

[17]:

from pygam import LinearGAM, f, s

from pygam.datasets import wage

X, y = wage(return_X_y=True)

## model

gam = LinearGAM(s(0) + s(1) + f(2))

gam.gridsearch(X, y)

## plotting

plt.figure()

fig, axs = plt.subplots(1, 3)

titles = ["year", "age", "education"]

for i, ax in enumerate(axs):

XX = gam.generate_X_grid(term=i)

ax.plot(XX[:, i], gam.partial_dependence(term=i, X=XX))

ax.plot(

XX[:, i], gam.partial_dependence(term=i, X=XX, width=0.95)[1], c="r", ls="--"

)

if i == 0:

ax.set_ylim(-30, 30)

ax.set_title(titles[i])

100% (11 of 11) |########################| Elapsed Time: 0:00:01 Time: 0:00:01

<Figure size 864x576 with 0 Axes>

Even though our model allows coefficients, our smoothing penalty reduces us to just 19 effective degrees of freedom:

[4]:

gam.summary()

LinearGAM

=============================================== ==========================================================

Distribution: NormalDist Effective DoF: 19.2602

Link Function: IdentityLink Log Likelihood: -24116.7451

Number of Samples: 3000 AIC: 48274.0107

AICc: 48274.2999

GCV: 1250.3656

Scale: 1235.9245

Pseudo R-Squared: 0.2945

==========================================================================================================

Feature Function Lambda Rank EDoF P > x Sig. Code

================================= ==================== ============ ============ ============ ============

s(0) [15.8489] 20 6.9 5.52e-03 **

s(1) [15.8489] 20 8.5 1.11e-16 ***

f(2) [15.8489] 5 3.8 1.11e-16 ***

intercept 0 1 0.0 1.11e-16 ***

==========================================================================================================

Significance codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

WARNING: Fitting splines and a linear function to a feature introduces a model identifiability problem

which can cause p-values to appear significant when they are not.

WARNING: p-values calculated in this manner behave correctly for un-penalized models or models with

known smoothing parameters, but when smoothing parameters have been estimated, the p-values

are typically lower than they should be, meaning that the tests reject the null too readily.

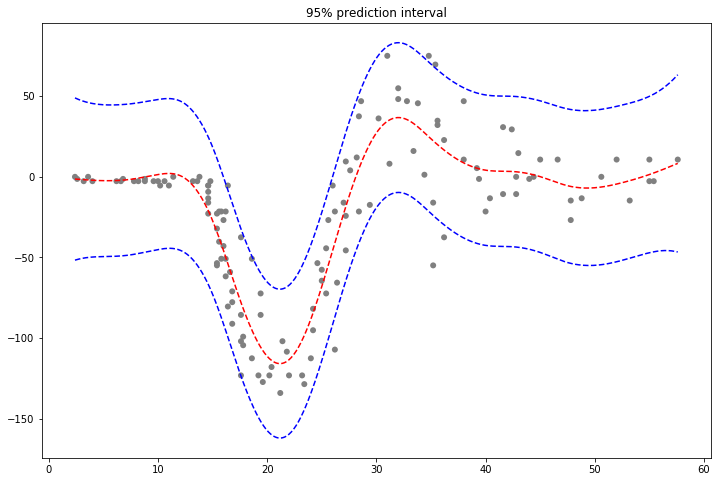

With LinearGAMs, we can also check the prediction intervals:

[56]:

from pygam import LinearGAM

from pygam.datasets import mcycle

X, y = mcycle(return_X_y=True)

gam = LinearGAM(n_splines=25).gridsearch(X, y)

XX = gam.generate_X_grid(term=0, n=500)

plt.plot(XX, gam.predict(XX), "r--")

plt.plot(XX, gam.prediction_intervals(XX, width=0.95), color="b", ls="--")

plt.scatter(X, y, facecolor="gray", edgecolors="none")

plt.title("95% prediction interval");

100% (11 of 11) |########################| Elapsed Time: 0:00:00 Time: 0:00:00

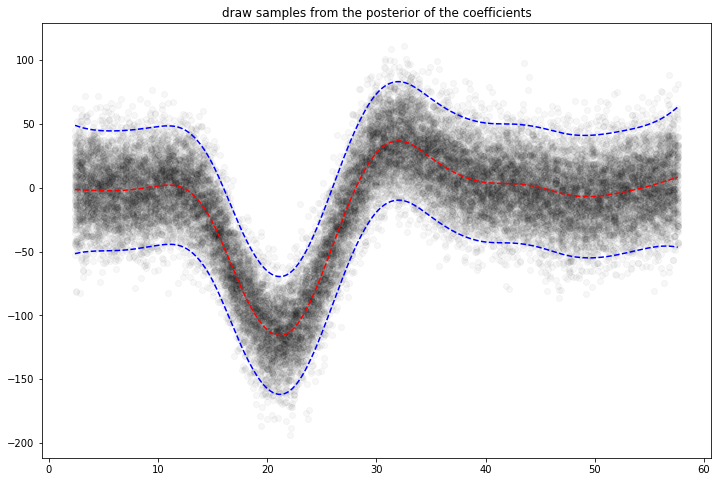

And simulate from the posterior:

[57]:

# continuing last example with the mcycle dataset

for response in gam.sample(X, y, quantity="y", n_draws=50, sample_at_X=XX):

plt.scatter(XX, response, alpha=0.03, color="k")

plt.plot(XX, gam.predict(XX), "r--")

plt.plot(XX, gam.prediction_intervals(XX, width=0.95), color="b", ls="--")

plt.title("draw samples from the posterior of the coefficients")

100% (11 of 11) |########################| Elapsed Time: 0:00:00 Time: 0:00:00

100% (11 of 11) |########################| Elapsed Time: 0:00:00 Time: 0:00:00

100% (11 of 11) |########################| Elapsed Time: 0:00:00 Time: 0:00:00

100% (11 of 11) |########################| Elapsed Time: 0:00:00 Time: 0:00:00

[57]:

Text(0.5,1,'draw samples from the posterior of the coefficients')

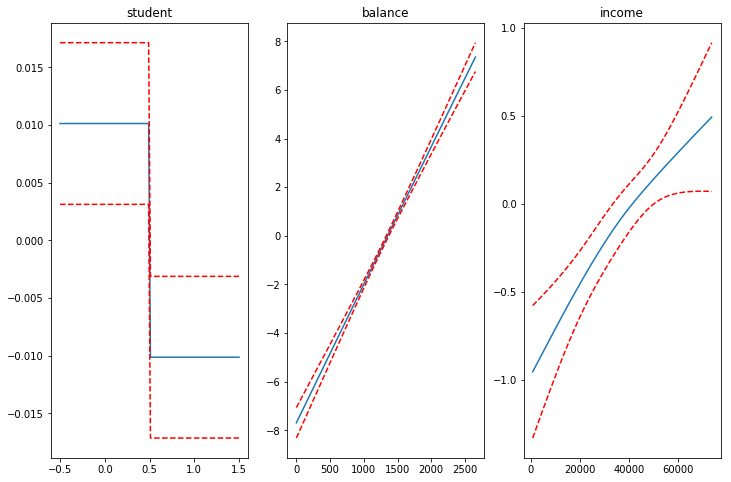

Classification#

For binary classification problems, we can use a logistic GAM which models:

[11]:

from pygam import LogisticGAM, f, s

from pygam.datasets import default

X, y = default(return_X_y=True)

gam = LogisticGAM(f(0) + s(1) + s(2)).gridsearch(X, y)

fig, axs = plt.subplots(1, 3)

titles = ["student", "balance", "income"]

for i, ax in enumerate(axs):

XX = gam.generate_X_grid(term=i)

pdep, confi = gam.partial_dependence(term=i, width=0.95)

ax.plot(XX[:, i], pdep)

ax.plot(XX[:, i], confi, c="r", ls="--")

ax.set_title(titles[i])

100% (11 of 11) |########################| Elapsed Time: 0:00:04 Time: 0:00:04

We can then check the accuracy:

[8]:

gam.accuracy(X, y)

[8]:

0.9739

Since the scale of the Binomial distribution is known, our gridsearch minimizes the Un-Biased Risk Estimator (UBRE) objective:

[9]:

gam.summary()

LogisticGAM

=============================================== ==========================================================

Distribution: BinomialDist Effective DoF: 3.8047

Link Function: LogitLink Log Likelihood: -788.877

Number of Samples: 10000 AIC: 1585.3634

AICc: 1585.369

UBRE: 2.1588

Scale: 1.0

Pseudo R-Squared: 0.4598

==========================================================================================================

Feature Function Lambda Rank EDoF P > x Sig. Code

================================= ==================== ============ ============ ============ ============

f(0) [1000.] 2 1.7 4.61e-03 **

s(1) [1000.] 20 1.2 0.00e+00 ***

s(2) [1000.] 20 0.8 3.29e-02 *

intercept 0 1 0.0 0.00e+00 ***

==========================================================================================================

Significance codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

WARNING: Fitting splines and a linear function to a feature introduces a model identifiability problem

which can cause p-values to appear significant when they are not.

WARNING: p-values calculated in this manner behave correctly for un-penalized models or models with

known smoothing parameters, but when smoothing parameters have been estimated, the p-values

are typically lower than they should be, meaning that the tests reject the null too readily.

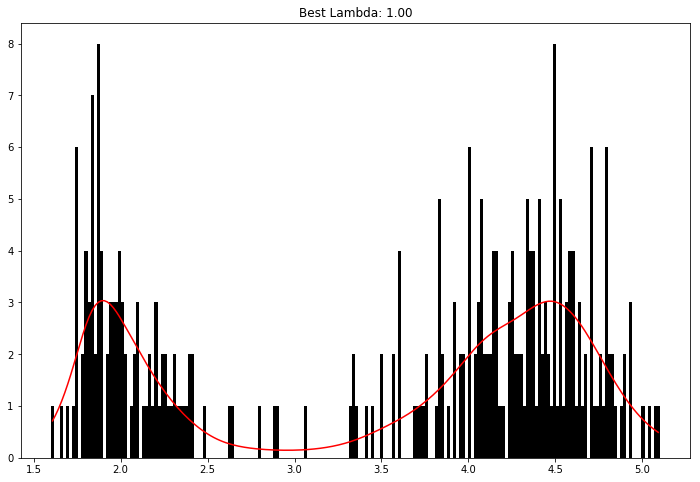

Poisson and Histogram Smoothing#

We can intuitively perform histogram smoothing by modeling the counts in each bin as being distributed Poisson via PoissonGAM.

[10]:

from pygam import PoissonGAM

from pygam.datasets import faithful

X, y = faithful(return_X_y=True)

gam = PoissonGAM().gridsearch(X, y)

plt.hist(faithful(return_X_y=False)["eruptions"], bins=200, color="k")

plt.plot(X, gam.predict(X), color="r")

plt.title(f"Best Lambda: {gam.lam[0][0]:.2f}");

100% (11 of 11) |########################| Elapsed Time: 0:00:00 Time: 0:00:00

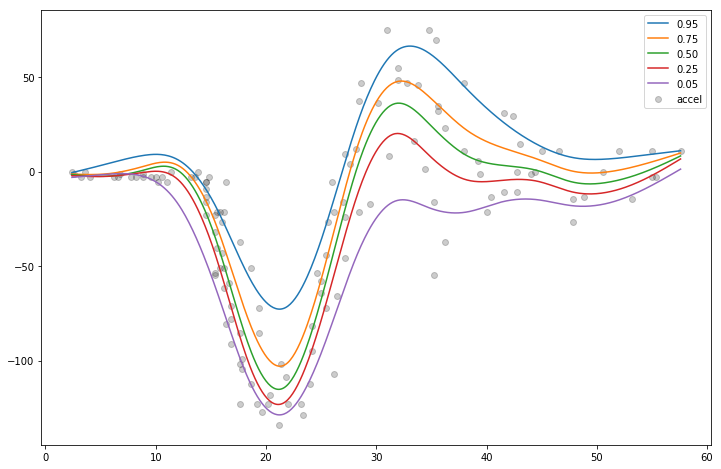

Expectiles#

GAMs with a Normal distribution suffer from the limitation of an assumed constant variance. Sometimes this is not an appropriate assumption, because we’d like the variance of our error distribution to vary.

In this case we can resort to modeling the expectiles of a distribution.

Expectiles are intuitively similar to quantiles, but model tail expectations instead of tail mass. Although they are less interpretable, expectiles are much faster to fit, and can also be used to non-parametrically model a distribution.

[52]:

from pygam import ExpectileGAM

from pygam.datasets import mcycle

X, y = mcycle(return_X_y=True)

# lets fit the mean model first by CV

gam50 = ExpectileGAM(expectile=0.5).gridsearch(X, y)

# and copy the smoothing to the other models

lam = gam50.lam

# now fit a few more models

gam95 = ExpectileGAM(expectile=0.95, lam=lam).fit(X, y)

gam75 = ExpectileGAM(expectile=0.75, lam=lam).fit(X, y)

gam25 = ExpectileGAM(expectile=0.25, lam=lam).fit(X, y)

gam05 = ExpectileGAM(expectile=0.05, lam=lam).fit(X, y)

100% (11 of 11) |########################| Elapsed Time: 0:00:00 Time: 0:00:00

[55]:

XX = gam50.generate_X_grid(term=0, n=500)

plt.scatter(X, y, c="k", alpha=0.2)

plt.plot(XX, gam95.predict(XX), label="0.95")

plt.plot(XX, gam75.predict(XX), label="0.75")

plt.plot(XX, gam50.predict(XX), label="0.50")

plt.plot(XX, gam25.predict(XX), label="0.25")

plt.plot(XX, gam05.predict(XX), label="0.05")

plt.legend()

[55]:

<matplotlib.legend.Legend at 0x7f58f816c3c8>

We fit the mean model by cross-validation in order to find the best smoothing parameter lam and then copy it over to the other models.

This practice makes the expectiles less likely to cross.

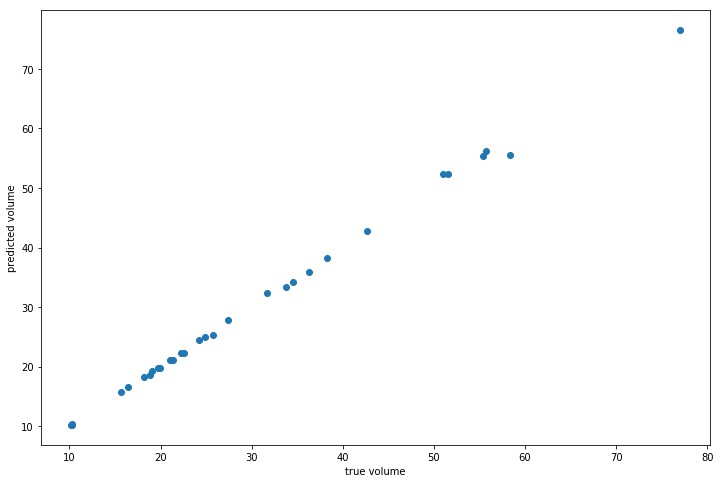

Custom Models#

It’s also easy to build custom models by using the base GAM class and specifying the distribution and the link function:

[27]:

from pygam import GAM

from pygam.datasets import trees

X, y = trees(return_X_y=True)

gam = GAM(distribution="gamma", link="log")

gam.gridsearch(X, y)

plt.scatter(y, gam.predict(X))

plt.xlabel("true volume")

plt.ylabel("predicted volume")

100% (11 of 11) |########################| Elapsed Time: 0:00:01 Time: 0:00:01

[27]:

Text(0,0.5,'predicted volume')

We can check the quality of the fit by looking at the Pseudo R-Squared:

[28]:

gam.summary()

GAM

=============================================== ==========================================================

Distribution: GammaDist Effective DoF: 25.3616

Link Function: LogLink Log Likelihood: -26.1673

Number of Samples: 31 AIC: 105.0579

AICc: 501.5549

GCV: 0.0088

Scale: 0.001

Pseudo R-Squared: 0.9993

==========================================================================================================

Feature Function Lambda Rank EDoF P > x Sig. Code

================================= ==================== ============ ============ ============ ============

s(0) [0.001] 20 2.04e-08 ***

s(1) [0.001] 20 7.36e-06 ***

intercept 0 1 4.39e-13 ***

==========================================================================================================

Significance codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

WARNING: Fitting splines and a linear function to a feature introduces a model identifiability problem

which can cause p-values to appear significant when they are not.

WARNING: p-values calculated in this manner behave correctly for un-penalized models or models with

known smoothing parameters, but when smoothing parameters have been estimated, the p-values

are typically lower than they should be, meaning that the tests reject the null too readily.

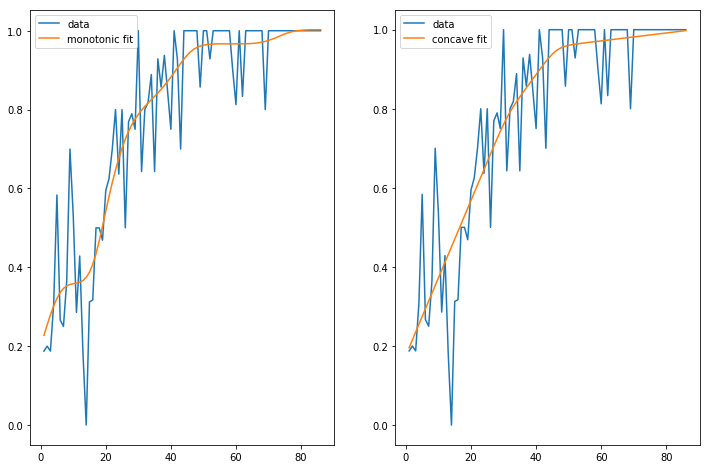

Penalties / Constraints#

With GAMs we can encode prior knowledge and control overfitting by using penalties and constraints.

Available penalties

second derivative smoothing (default on numerical features)

L2 smoothing (default on categorical features)

Available constraints

monotonic increasing/decreasing smoothing

convex/concave smoothing

periodic smoothing [soon…]

We can inject our intuition into our model by using monotonic and concave constraints:

[29]:

from pygam import LinearGAM, s

from pygam.datasets import hepatitis

X, y = hepatitis(return_X_y=True)

gam1 = LinearGAM(s(0, constraints="monotonic_inc")).fit(X, y)

gam2 = LinearGAM(s(0, constraints="concave")).fit(X, y)

fig, ax = plt.subplots(1, 2)

ax[0].plot(X, y, label="data")

ax[0].plot(X, gam1.predict(X), label="monotonic fit")

ax[0].legend()

ax[1].plot(X, y, label="data")

ax[1].plot(X, gam2.predict(X), label="concave fit")

ax[1].legend()

[29]:

<matplotlib.legend.Legend at 0x7fa3970b19e8>

API#

pyGAM is intuitive, modular, and adheres to a familiar API:

[30]:

from pygam import LogisticGAM, f, s

from pygam.datasets import toy_classification

X, y = toy_classification(return_X_y=True, n=5000)

gam = LogisticGAM(s(0) + s(1) + s(2) + s(3) + s(4) + f(5))

gam.fit(X, y)

[30]:

LogisticGAM(callbacks=[Deviance(), Diffs(), Accuracy()],

fit_intercept=True, lam=[0.6, 0.6, 0.6, 0.6, 0.6, 0.6],

max_iter=100,

terms=s(0) + s(1) + s(2) + s(3) + s(4) + f(5) + intercept,

tol=0.0001, verbose=False)

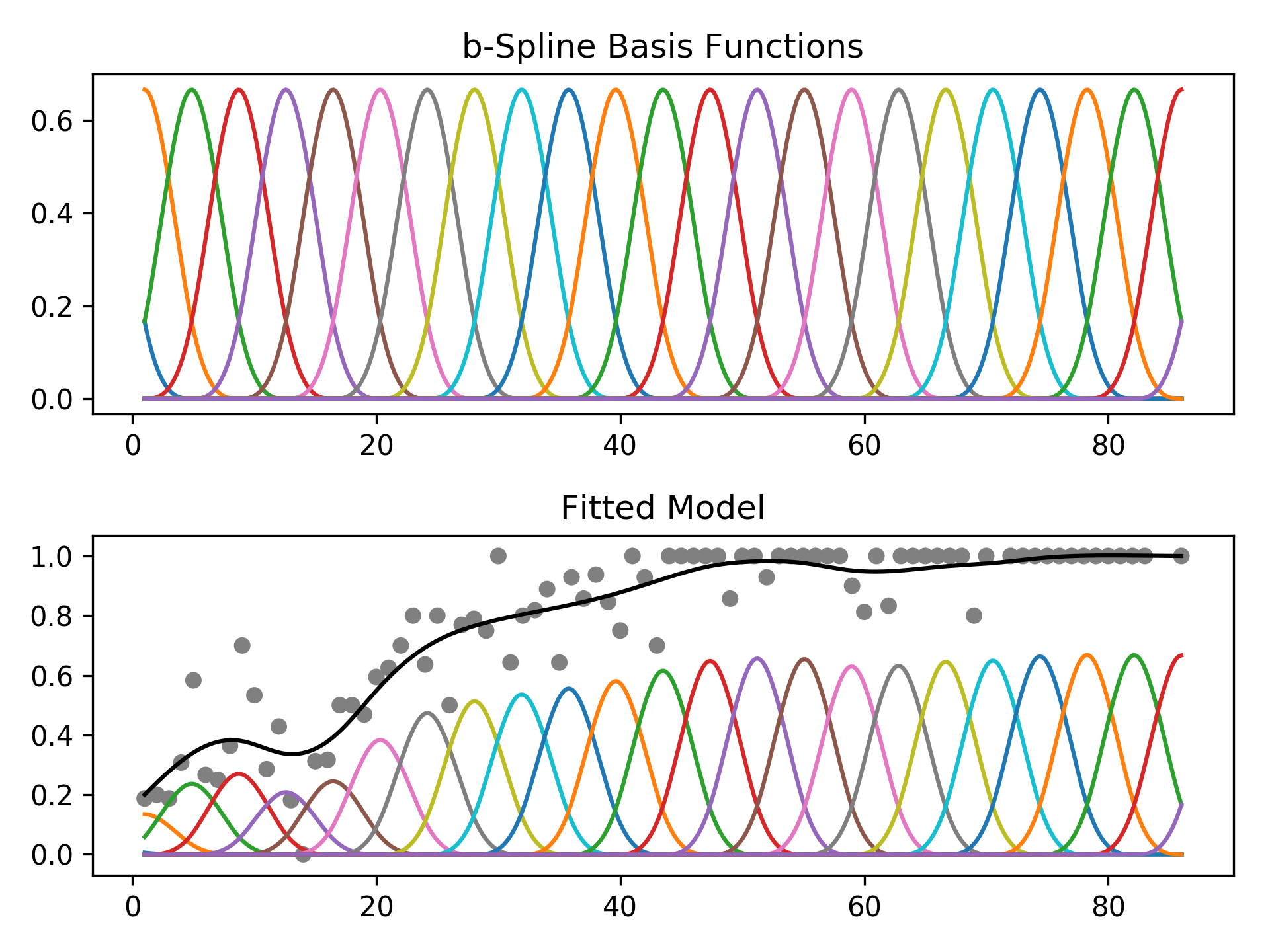

Since GAMs are additive, it is also super easy to visualize each individual feature function, f_i(X_i). These feature functions describe the effect of each X_i on y individually while marginalizing out all other predictors:

[31]:

plt.figure()

for i, term in enumerate(gam.terms):

if term.isintercept:

continue

plt.plot(gam.partial_dependence(term=i))

Current Features#

Models#

pyGAM comes with many models out-of-the-box:

GAM (base class for constructing custom models)

LinearGAM

LogisticGAM

GammaGAM

PoissonGAM

InvGaussGAM

ExpectileGAM

Terms#

l()linear termss()spline termsf()factor termste()tensor productsintercept

Distributions#

Normal

Binomial

Gamma

Poisson

Inverse Gaussian

Link Functions#

Link functions take the distribution mean to the linear prediction. These are the canonical link functions for the above distributions:

Identity

Logit

Inverse

Log

Inverse-squared

Callbacks#

Callbacks are performed during each optimization iteration. It’s also easy to write your own.

deviance - model deviance

diffs - differences of coefficient norm

accuracy - model accuracy for LogisticGAM

coef - coefficient logging

You can check a callback by inspecting:

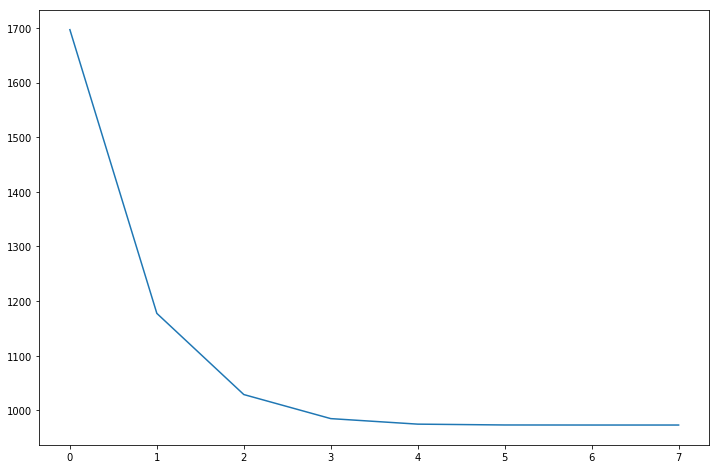

[32]:

_ = plt.plot(gam.logs_["deviance"])

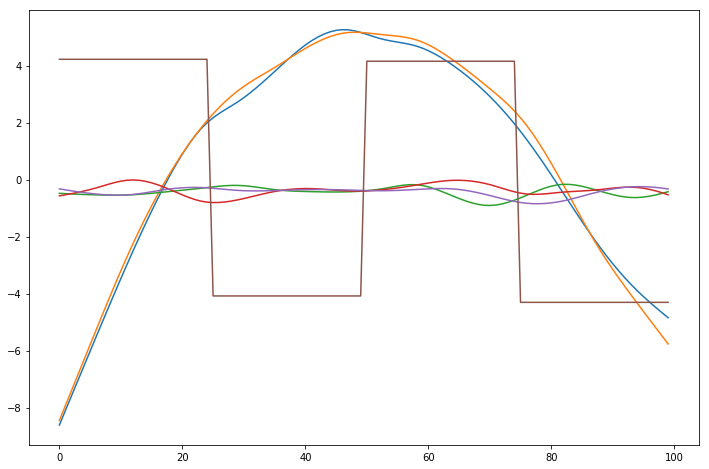

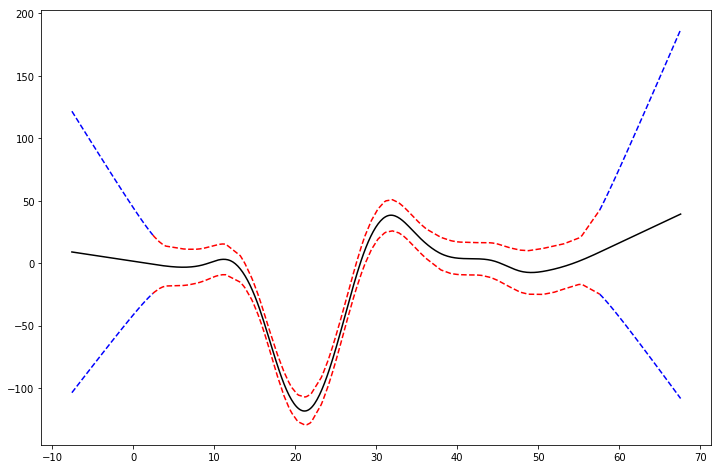

Linear Extrapolation#

[ ]:

import numpy as np

from pygam import LinearGAM

from pygam.datasets import mcycle

X, y = mcycle()

gam = LinearGAM()

gam.gridsearch(X, y)

XX = gam.generate_X_grid(term=0)

m = X.min()

M = X.max()

XX = np.linspace(m - 10, M + 10, 500)

Xl = np.linspace(m - 10, m, 50)

Xr = np.linspace(M, M + 10, 50)

plt.figure()

plt.plot(XX, gam.predict(XX), "k")

plt.plot(Xl, gam.confidence_intervals(Xl), color="b", ls="--")

plt.plot(Xr, gam.confidence_intervals(Xr), color="b", ls="--")

_ = plt.plot(X, gam.confidence_intervals(X), color="r", ls="--")

100% (11 of 11) |########################| Elapsed Time: 0:00:00 Time: 0:00:00

References#

- Simon N. Wood, 2006Generalized Additive Models: an introduction with R

- Hastie, Tibshirani, FriedmanThe Elements of Statistical Learning

- James, Witten, Hastie and TibshiraniAn Introduction to Statistical Learning

- Paul Eilers & Brian Marx, 1996 Flexible Smoothing with B-splines and Penalties

- Kim Larsen, 2015GAM: The Predictive Modeling Silver Bullet

- Deva Ramanan, 2008UCI Machine Learning: Notes on IRLS

- Paul Eilers, Brian Marx, and Maria Durbán, 2015Twenty years of P-splines

- Keiding, Niels, 1991Age-specific incidence and prevalence: a statistical perspective